Download Job Order Costing: A Comprehensive Guide to Cost Accumulation Methods and more Assignments Accounting in PDF only on Docsity!

CHAPTER 5

DISCUSSION QUESTIONS

5-

Q5-1. The cost attached to a product is an amount assigned by the costing methods used—an amount controlled by the circumstances, assumptions, and limitations of the method under which it was compiled. Product costs are composites of historical outlay that have, perhaps, been modified by estimates or stan- dards, by processes assigning or prorating expenditures to periods, or by tracing the direct costs and allocating the indirect costs to particular products so that the total period outlay is spread over the aggregate output. Despite these shortcomings, product costs are useful in costing inventories, comparing prices and total unit cost, measuring current profit or loss, and indicating the minimum cost below which a sales price cannot go in the long run. Some confusion will result at times in using cost information in making manage- ment decisions unless information relevant only to the decision is used. Q5-2. The primary objective in job order costing is to determine the cost of materials, labor, and factory overhead used to produce a specific order or contract. Cost estimates are made when the order is taken, and the job order procedures are designed to reveal costs as the order goes through production, thereby giving an opportunity to control costs. Q5-3. The type of cost accumulation method used by a company will be determined by the type of manufacturing operations performed. A manufacturing company should use process cost accumulation for product costing pur- poses when like units are continuously mass produced; when custom-made or unique goods are produced, job order costing would be more appropriate. Process costing is often used in industries such as chemicals, food processing, oil, mining, rubber, and electrical appliances. With a continuous mass produc- tion of like units, the center of attention is the individual process (usually a department).

The unit costs by cost category as well as total unit cost for each process (department) are necessary for product costing purposes. Q5-4. A job order cost sheet is used: (a) to keep track of the direct materials and direct labor used on a job plus an appro- priate share of factory overhead; (b) to compare actual costs to estimated costs; (c) as a subsidiary ledger for the work in process account. Q5-5. The work in process account is a control account in the general ledger, reflecting total costs assigned or applied to jobs. The individ- ual job cost sheets form the work in process account’s subsidiary ledger, indicating the direct materials, direct labor, and factory over- head charged to each job. Q5-6. Job order cost sheets serve a control func- tion. Comparisons are made between esti- mates of job costs and costs actually accumulated for the job. In addition, cost con- trol is enhanced by accumulating direct mate- rials and labor as well as factory overhead costs by cost centers or departments, and by comparing the actual costs to cost center budgets. Q5-7. Actual factory overhead consists of the day- by-day costs that are actually experienced and incurred by the company. Applied factory overhead is the overhead charged to jobs based on the predetermined factory overhead rate. This rate is created by dividing total esti- mated overhead by total estimated number of units (or any other appropriate base). The dif- ference between actual and applied factory overhead is the over- or underapplied factory overhead. Q5-8. The characteristic of a service business that makes likely the use of job order costing is that all jobs are not alike and cost information for each job is desired.

EXERCISES

E5-1 Job 5575 Direct material............................................................... $24, Direct labor.................................................................... 22, Applied overhead ......................................................... 10, Total job cost ....................................................... $56,

E5-2 Job 5576 Direct material............................................................... $ 4, Direct labor.................................................................... 2, Applied overhead ......................................................... 2, Cost to date.......................................................... $ 9,

E5-

(1) The amount of direct labor in finished goods: Finished goods ............................................................. $37, Materials included in finished goods ($15,500 – $3,200) 12, Direct labor and factory overhead in finished goods $25,

Let X = direct labor in finished goods 1.8X = $25,200 direct labor and factory overhead in finished goods X = $14,000 direct labor in finished goods

(2) The amount of factory overhead in finished goods: X = $14, .8X = .8($14,000) .8X = $11,200 factory overhead in finished goods

E5- (1) December materials used: Materials inventory, December 1............... $ 8, Materials purchased ................................... $87, Freight-in .................................................... 1,500 88,

Materials available ...................................... $96, Materials inventory, December 31............. 6, $90,

Factory overhead charged to work in process Direct labor charged to woork in process

5-2 Chapter 5

E5-5 Materials:

Direct Materials Direct Labor Applied Factory Overhead Date Date Date

(2) Cost of goods manufactured:

(3) Cost of goods sold:

P5-2 (Concluded)

(3) Cost of goods manufactured = cost of jobs finished in April. Job 205: Direct material ............................ $ 2, Direct labor ................................. 2,100 (105 direct labor hours × $20) Applied overhead ....................... 1,680 (105 direct labor hours × $16) Total Job 205........................... $ 6,

Job 202 ................................................. 9,550 (see requirement (2)) Job 204 ................................................. 6, Job 207 ................................................. 5, Total ......................................... $28,

(4) Actual overhead (1,375 + 2,500 + 2,700 + 2,790) ....... $9, Applied overhead: Jobs 202, 203, 205, 206 (330* hours × $16) ....... $ 5, Job 207 ................................................................. 1, Job 204 ($1,760 – $960) ...................................... 800 Total applied overhead............................... 7, Underapplied................................................................. $1, *100 + 75 + 105 + 50

(5) Jobs 201, 202, and 205 were sold. Their costs are $8,450 + $9,550 + $6,280 = $24,280. Sales ($24,280 × 1.5) .................................................... $36, Cost of goods sold....................................................... (24,280) Underapplied overhead................................................ (1,765) Gross profit for April .................................................... $10,

P5-

Finished Goods Work in Process

Bal. 80,000 360,000 Bal. 20,000 (i) 320, (i) 320,000 (c) 150, 400,000 (e) 80, 40,000 100,000 * 350, 30,

*$330,000 – $80,000 = $250,000 direct labor and factory overhead. Factory overhead is 150% of direct labor, therefore, direct labor is $100,

5-10 Chapter 5

P5-3 (Concluded)

Materials Cost of Goods Sold

Bal. 15,000 (e) 80,000 360, (b) 100,000 12, 115,000 92, 23,

Factory Overhead Control Applied Factory Overhead

(d) 60,000 (c) 150, 12, 75, 147,

Accounts Payable Accrued Payroll

(f) 102,000 Bal. 7,000 (j) 172,000 Bal. 11, 100,000 175, 107,000 186, 5,000 14,

Accounts Receivable Sales

Bal. 45,000 (h) 480,000 (a) 500,000** (a) 500, 545, 65,

**Cost of goods sold is 72% of sales (100% – 28%).

(1) Materials purchased—$100, (2) Cost of goods sold—$360, (3) Finished goods ending inventory—$40, (4) Work in process ending inventory—$30, (5) Direct labor cost—$100, (6) Applied factory overhead—$150, (7) Over or underapplied factory overhead—$3,000 overapplied (8) Closed out to the cost of goods sold account

CGA-Canada (adapted). Reprint with permission.

Chapter 5 5-

P5-4 (Concluded)

(2) COLUMBUS COMPANY Income Statement For Month Ended October 31 Sales ................................................................... $144, Less sales returns and allowances ................. 1, Net sales ........................................................... $143, Less cost of goods sold ................................... 76, Gross profit ........................................................ $ 67, Less commercial expenses: Marketing expense ................................... $25, Depreciation—building............................. 30 Depreciation—office equipment.............. 16 $25, Administrative expense ........................... $19, Depreciation—building............................. 20 Depreciation—office equipment.............. 24 19,744 44, Income before income tax ................................ $ 22,

(3) Amount of over- or underapplied factory overhead: Actual factory overhead: Factory overhead paid ............................. $20, Indirect materials ...................................... 3, Depreciation—building............................. 150 Depreciation—machinery and equipment......................................... 800 Indirect labor ............................................. 4,400 $29, Applied factory overhead.................................. 27, Underapplied factory overhead........................ $ 1,

Chapter 5 5-

P5-

(1) LOGANVILLE CANNING COMPANY

Balance Sheet December 31, 20B Assets

Current assets: Cash ........................................................... $19, Accounts receivable ................................. 10, Inventories: Finished goods ................................ $4, Work in process ............................... 1, Materials ........................................... 2,000 7, Prepaid expenses ..................................... 500 Total current assets......................... $36, Property, plant, and equipment (net) ............... 26, Total assets ........................................................ $62,

Liabilities

Current liabilities ............................................... $17,

Stockholders’ Equity

Common stock................................................... $30, Retained earnings.............................................. 15,

Total stockholders’ equity................................. 45, Total liabilities and stockholders’ equity......... $62,

5-14 Chapter 5

(1) and (2) JUAREZ INC. Job Order Cost Sheets To Post Beginning Inventory Data

(j) Completed and transferred Completed and trans- Still in to warehouse ferred to warehouse process

P5-6 (Concluded)

P5-7 (Concluded)

(2) The total cost of each job at the end of March:

(1) and (3) GENERAL LEDGER Accumulated Depreciation—

- Beginning inventory $ - Materials available for use.................................. $ Purchases............................................................. 336 (1) - Less ending inventory - Materials used...................................................... $

- Factory overhead ($225 × .6) Direct labor (($686 – $326) ÷ 1.6) 225 (2)

- Total manufacturing cost............................................. $

- Add work in process, beginning inventory................ - $

- Less work in process, ending inventory

- Add finished goods, beginning inventory.................. Cost of goods manufactured $736 (3)

- Cost of goods available for sale $

- Less finished goods, ending inventory......................

- E5- Cost of goods sold....................................................... $716 (4)

- (1) Materials $13,

- Direct labor 15,

- Molding (1,000 DLH × $2.70)............................... 2, Factory overhead:

- Decorating ($6,000 × 35%) 2,

- Estimated cost to produce $32,

- (2) Materials $13,

- Direct labor.................................................................... 15,

- Estimated prime cost $28,

- (3) Direct labor.................................................................... $15,

- Factory overhead ($2,700 + $2,100) 4,

- Estimated conversion cost $19,

- (4) Estimated cost to produce (requirement (1)) $32,

- Markup ($32,800 × 35%) 11,

- Bid price $44,

- 5-4 Chapter

- E5- - Job Order Cost Sheet—Job (1) KEMP MACHINE WORKS

- 9/14 $ 600 9/20 90 $6.20 $ 558 9/20 10 $80 $ Issued Amount (Week of) Hours Rate Cost (Week of) Hours Rate Cost

- 9/20 331 9/26 70 7.30

- 9/22

- $1,131 $1,069 $

- Direct materials.................................................... $1, (2) Sales price of Job 909, contracted a markup of 65% of cost:

- Direct labor........................................................... 1,

- Applied factory overhead

- Total factory cost................................................. $3,

- Markup 65% of production cost......................... 1,

- Sales price............................................................ $4,

- E5-

- (1) Work in Process (35,000 + 45,000 + 55,000) 135, Debit Credit - Materials 135,

- (2) Work in Process (45,000 + 40,000 + 35,000) 120, - Payroll 120,

- (3) Work in Process (36,000 + 32,000 + 28,000) 96, - Factory Overhead Control 96,

- (4) Finished Goods (156,000 + 132,000)........................... 288, - Work in Process................................................... 288,

- Chapter 5 5-

- E5-9 (a) Materials 35, - Accounts Payable 35, - (b) Work in Process................................................... 8, - Factory Overhead Control 2, - Materials 10, - (c) Payroll 9, - Accrued Payroll 9, - Work in Process................................................... 7, - Factory Overhead Control 1, - Payroll 9, - (d) Factory Overhead Control 1, - Factory Equipment 1, Accumulated Depreciation— - (e) Work in Process (1,830 × 66 2/3%) 1, - Applied Factory Overhead......................... 1, - Finished Goods (1,450 + 1,830 + 1,220) 4, - Work in Process.......................................... 4, - (f) Factory Overhead Control 1, - Accounts Payable 1, - (g) Accounts Receivable 5, - Sales 5, - Cost of Goods Sold............................................. 4, - Finished Goods 4,

- E5-

- Inv. 10,000 WIP 110,000 Inv. 30,000 FG 300, Materials Work in Process

- Purch. 138,000 Materials 110, - 38,000 overhead 90, 148,000 Factory - Labor 180, - 410, - 110,

- Inv. 50,000 CGS 205,000 FG 205, Finished Goods Cost of Goods Sold

- WIP 300, - 350,

- 5-6 Chapter CGA-Canada (adapted). Reprint with permission.

- E5-

- (1) Work in Process............................................................ 21,112.

- Materials 11,250.

- Payroll 3,945.

- Applied Factory Overhead.................................. 5,917.

- (2) Finished Goods 21,112.

- Work in Process................................................... 21,112.

- Chapter 5 5-

- P5- PROBLEMS

- Materials $ 60, (1) Total cost of work put into process:

- Labor: Grinding (8,000 hrs. × $5.60) 44, - Machining (4,600 hrs. × $6) 27,

- Factory overhead: Grinding (8,000 hrs. × $6)..... 48, - Machining (4,600 hrs. × $8) 36, - $217,

- (from requirement (1)) $217, Total cost of work put into process

- Work in process, beginning inventory 15, - $232,

- Work in process, ending inventory.................... 17, - $214,

- (from requirement (2)) $214, Cost of goods manufactured

- Finished goods, beginning inventory................ 22, - $236,

- Finished goods, ending inventory 17, - $219,

- Labor: Grinding (8,000 hrs. × $5.60) $ 44, (4) Conversion cost:

- Machining (4,600 hrs. × $6) 27,

- Factory overhead: Grinding (8,000 hrs. × $6)..... 48, - Machining (4,600 hrs. × $8) 36, - $157,

- Materials put into process.................................. $ 60, (5) Cost of materials purchased:

- Add materials, ending inventory 18, - $ 78,

- Less materials, beginning inventory 19, - $ 59,

- 5-8 Chapter

- Sales $60, For Year Ended December 31, 20B - Inventory, January 1..................................... $ 4, Materials: - Purchases 15, - Materials available for use........................... $19, - Less inventory, December 31 2, - Materials consumed..................................... $17,

- Direct labor........................................................... 9,

- Applied factory overhead 9,

- Total manufacturing cost.................................... $35,

- Add work in process inventory, January 1 2, - $37,

- Less work in process inventory, December 31. 1,

- Cost of goods manufactured $36,

- Add finished goods inventory, January 1 6,

- Cost of goods available for sale $42,

- Less finished goods inventory, December 31 4,

- Cost of goods sold.............................................. $38,

- Add underapplied factory overhead 2,

- Cost of goods sold—adjusted 40,

- Gross profit $20,

- Marketing expense $ 6, Less commercial expenses:

- Administrative expense 9,000 15,

- Income before income tax $ 5,

- Chapter 5 5-

- P5- - Job 621 Job 622 Job March 1, 20–

- Materials $ 2,800 $ 3,400 $ 1,

- Labor 2,100 2,700 1,

- Factory Overhead 1,680 2,160 1,

- Total $ 6,580 $ 8,260 $ 4,

- (b) M......... 5,300 7,400 5,

- (f) L.......... 6,420 8,160 6, (c) M (400)

- (h) OH 5,136 6,528 5,

- Total $23,436 $29,948 $21,

- (a) Materials 19,000. (2) Dr. Cr. - Accounts Payable 19,000.

- (b) Work in Process................................................... 18,600.

- Factory Overhead Control 2,400.

- (c) Materials 600. - Work in Process 400. - Factory Overhead Control 200.

- (d) Accounts Payable 800. - Materials 800.

- (e) Payroll 38,000. - Accrued Payroll 38,000.

- (f) Work in Process................................................... 20,900.

- Factory Overhead Control 7,600.

- Marketing Expenses Control 5,700.

- Administrative Expenses Control 3,800.

- (g) Factory Overhead Control 9,404. - Accounts Payable 7,154. - Building & Equipment 2,000. Accumulated Depreciation—Factory - Prepaid Insurance 250.

- 5-16 Chapter - (h) Work in Process................................................... 16,720. Dr. Cr. - Factory Overhead) 16,720. Factory Overhead Control (or Applied - (i) Finished Goods 53,384. - Work in Process 53,384. - Sales 74,738. (j) Accounts Receivable 74,738.00* - Cost of Goods Sold............................................. 53,384. - Finished Goods 53,384. - (k) Cash 69,450. - Accounts Receivable 69,450. - * ($53,384 × 40%) + $53,384 = $74,

- 3/1 Bal. 17,000 (b) 21,000 3/1 Bal. 19,070 (c) Materials Work in Process

- (a) 19,000 (d) 800 (b) 18,600 (i) 53,

- (c) 600 21,800 (f) 20,900 53, - 36,600 (h) 16,

- 3/1 Bal. 15,000 (j) 53, Finished Goods

- (i) 53, - 68,

- 15, - Schedule of Inventories, March (3) JUAREZ INC.

- Materials $14,

- Work in Process (Job 623)............................................................................... 21,

- Finished Goods 15,

- Total $51,

- Chapter 5 5-

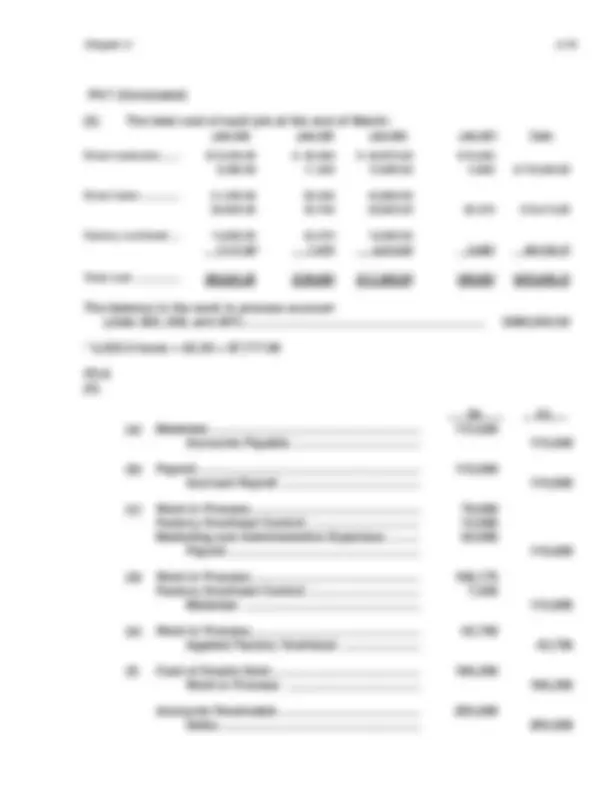

- Direct materials $15,230.00 $ 40,450 $ 60,875.00 $16, Job 204 Job 205 Job 206 Job 207 Total - 9,480.00 11,320 10,490.00 5,800 $170,285.

- Direct labor 21,430.00 55,240 43,860. - 26,844.00 22,750 28,920.00 20,370 219,414.

- Factory overhead 13,800.00 22,370 19,366. - 7,717.65* 7,475 8,314.50 6,693 85,736.

- Total cost $94,501.65 $159,605 $171,825.50 $49,503 $475,435.

- (Jobs 205, 206, and 207)......................................................................... $380,933. The balance in the work in process account

- 3,355.5 hours × $2.30 = $7,717.

- P5- - (a) Materials 115, Dr. Cr. - Accounts Payable 115, - (b) Payroll 110, - Accrued Payroll 110, - (c) Work in Process................................................... 78, - Factory Overhead Control 12, - Marketing and Administrative Expenses 20, - Payroll 110, - (d) Work in Process................................................... 108, - Factory Overhead Control 7, - Materials 115, - (e) Work in Process................................................... 42, - Applied Factory Overhead 42, - (f) Cost of Goods Sold............................................. 190, - Work in Process 190, - Accounts Receivable 255, - Sales 255,

- Chapter 5 5- - (g) Cash 247, P5-8 (Continued) - Sales Discounts................................................... 13, - Accounts Receivable 260, - (h) Marketing and Administrative Expenses 15, - Factory Overhead Control 24, - Cash 37, - Accumulated Depreciation—Machinery 2, - (i) Accounts Payable 85, - Cash 85, - (j) Applied Factory Overhead.................................. 42, - Factory Overhead Control 42, - Cost of Goods Sold............................................. 1, - Factory Overhead Control 1,

- 1/1 Bal. 47,000 (h) 37,680 1/1 Bal. 21,500 (d) 115, Cash Materials

- (g) 247,000 (i) 85,000 (a) 115, - 294,000 122,680 136,

- 1/1 Bal. 50,000 (g) 260,000 1/1 Bal. 45, Accounts Receivable Machinery

- (f) 255, - 305, - 45,

- 1 /1 Bal. 32,500 1/1 Bal. 10, Finished Goods Machinery - (h) 2, - 12,

- 1/1 Bal. 7,500 (f) 190,350 (i) 85,000 1/1 Bal. 58, Work in Process Accounts Payable

- (c) 78,000 (a) 115,

- (d) 108,175 173,

- (e) 42,750 88, - 236, - 46,

- 5-20 Chapter